Follow Us

Follow Us

https://www.desidime.com/news/home-loans-emi-how-to-save-on-your-emi-61ca8253-1cd5-4261-90f7-3e0af36a7671?page=1#post_8212499

someone pls tell me how to save/bookmark a good topic like this

Having a home loan and finding it harder to pay your regular EMI due to salary cuts or loss in business or personal income? Covid-19 has bought forward some of the most unexpected financial planning problems and you are not alone, if you are facing problems or struggling to pay your Home Loan EMIs. We have highlighted many ways using which you can manage your EMI better and stay on top of your Credit Score and keep your Credit history clean.

The “Debt Trap” is the worst thing you would want to get into during this recession-like situation as interest rates can quickly pile up along with Late Fees, Penalty etc making a very horrendous situation to be in. We have put down concrete steps and suggestions and we assure you that it will be well spent 90 minutes to get things in order and save Lakhs of Rupees over the next 10-15 years.

Every Home loan EMI has 2 components - Principal and Interest Component. In the earlier years of your loan, you end up paying a higher interest component and a much lower principal component. As your principal keeps reducing, your interest component also keeps going down. The Home Loan is given to you for a fixed number of years, often called “Loan Tenure”. And the final element which matters the most is Interest Rate or Home Loan Rate. Interest rate can either be Fixed rate or Floating rate. Fixed rate means that your interest rate would stay the same irregardless of any changes by RBI. Floating Rate usually means that your interest rates are revised every quarter based on the Repo rate (Rate decided by RBI). All these basic elements are linked to each other and you need to understand these elements first by downloading your latest Home Loan statement.

If you start repaying a higher amount compared to your EMI, your loan Tenure automatically decreases and so does your future interest (as you are paying off additional principal). Similarly, if the interest rate is reduced on your loan and you continue to pay the original EMI, your remaining loan tenure decreases at a faster rate.

If you read news regularly, you might be aware that RBI has been aggressively cutting down Repo Rates every month to bring in more liquidity in Indian market, given the recession-like situation. In May 2020, RBI cut the repo rate from 4.4 percent to 4 percent. That’s a 40 basis point rate cut. This follows the rate reduction of 25 basis points in mid-April and 75 basis points on March 27. However, these rate cuts are meant for Banks and All Banks will not aggressively pass the same rate cuts to all customers.

You will have to do some work! Banks would obviously like to make some money. While they may quickly hike interest rates when Repo rates are increased, It’s very common for Banks to delay when it comes to slashing interest rates and passing on the benefits to customers. The usual strategy of Private banks is to slowly watch PSU Banks like SBI etc for rate cuts and then they follow their footsteps, earning good interest meanwhile.

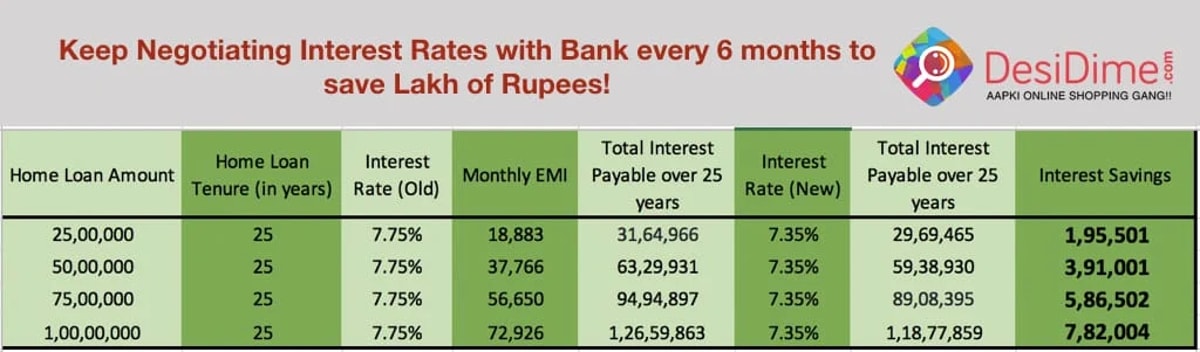

Let’s understand the maths first behind the rate cut and how a 0.25% lower interest rate can help you to save Lakhs of rupees over the entire loan tenure.

Let's assume that you have taken a Home Loan of 50 Lakh rupees for a tenure of 25 years and your current interest rate is 7.75%. If you switch to a bank offering 7.35% interest rate or convince your existing bank to give you a lower interest rate, You end up saving Rs. 3,91,000. Yes, A whopping Rs. 3.9 Lakh is straight in your pocket

A wise Dimer "@nhavale":https://www.desidime.com/users/85388 also shared a very important thing in comments: One can reduce tenure also if EMI is affordable and that can save upto Rs. 10.23 Lakh in the above example. So, if you are keeping money in FD, then obviously you must reduce tenure and pay away as much as you can.

So, Do some homework on popular websites like Bank Bazaar or SwitchMe and Call your bank and explain to them how you are getting lower rates with other banks and you are considering switching the Home Loan. No bank would like to lose a good customer and they would generally give you the best possible rates. It may not be exactly the same as the lowest available on BankBazaar but you must also consider switching costs etc. It’s not advisable to switch banks or do a balance transfer until you are saving more than 1% in interest rate.

Also, Do not forget that it's not a one-time exercise. You need to analyze/research this every 6 months and you are bound to save some serious money!

If you had taken Home Loan after July 1, 2010 but before April 1, 2016, then there is a very high likelihood that your Loan rate is linked to Lending Bank’s Base Rate. If you are under the Base Rate Regime, it's likely that your interest rate might be upwards of 10%.

A new regime of lending called marginal cost of funds based lending rate (MCLR) was announced and implemented by RBI for all loans, including Home Loans, disbursed after April 1 2016. The new MCLR regime makes it compulsory for the Banks to pass on rate changes to customers faster without any request by the customer. One of the most favourable decisions made by RBI keeping end-consumers in mind.

So now you must be wondering, Can I not take benefits of MCLR if I took Home Loan before 2016? Do I need to call the Bank every 6 months? RBI in its guidelines have made it very clear that customers must be allowed to switch to MCLR from Base Rate without paying any additional Fees. So you have full legal right to switch your home loan to MCLR rate by just calling the bank and requesting the same. All Banking executives are normally aware about it and they will guide you. Obviously, you must only do this if your existing rate is higher than MCLR Rate.

MCLR rates are released by RBI every month here or you can also see the MCLR rates for popular banks on BankBazaar.

If your loan is in the BPLR (Benchmark Prime Lending Rate) regime, you can still call and switch to MCLR rate if it makes sense financially. Simply ask your banker about the current MCLR rate vs your interest rate and they will always guide you.

If you had taken a loan from a Housing Finance Company (HFC) and not a bank, then as per RBI regulations, HFC are not obliged to switch customers to MCLR. In such cases, you can consider doing your Balance Transfer to another bank and there are many websites like BankBazaar or SwitchMe to help you transfer.

The risk with MCLR is that in events of rapidly falling interest rates, the banks may reset the interest rate after 12 months if it's linked to the 12 month MCLR rate. So one need to negotiate to link their loan to quarterly or 6 months MCLR to really avail the benefits.

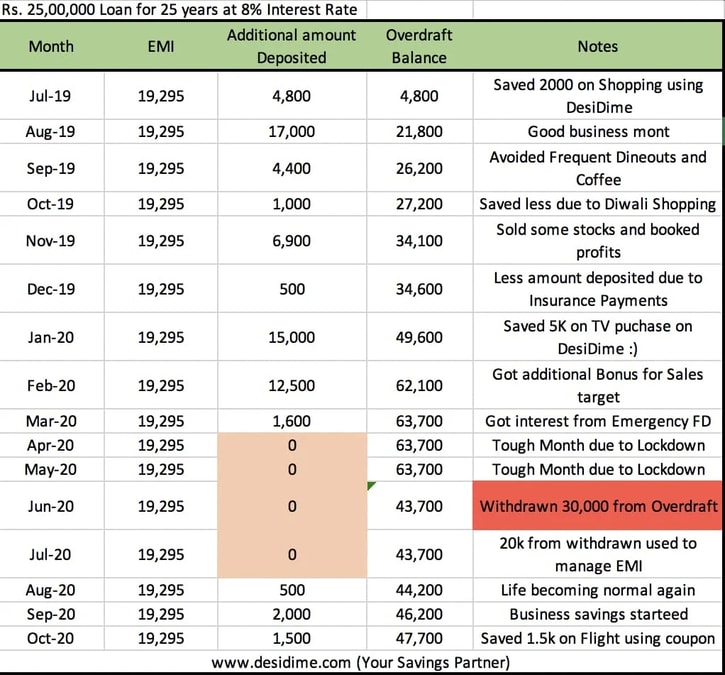

If you are not salaried and running a business, there is a likelihood that your income is not steady and keeps varying every month. In such cases, it often happens that during your good business months, you might be over-spending on luxuries or discretionary spends. Or you might simply be depositing the money in FD while paying a higher interest rate for your Home Loan. During an unplanned crisis like Covid19 or say floods or earthquakes or simply cyclical nature of your business, one can experience a huge drop in business income. If the above resonates with you, then you must consider opting for Home Loan Overdraft Facility. In simple terms, You simply pay more than your EMI amount during your good months and the excess amount paid is deposited in the Overdraft account. The amount also offsets your principal amount which helps you to keep reducing your Interest component every month or total interest payable.

During a crisis or say a bad few months, you can also withdraw the overdraft money to support you and your family. The overdraft money can also be used to pay EMI after withdrawal in case you are struggling with your EMI payments too. The beauty of Home Loan Overdraft Facility is the discipline it brings to you to prepare for worst-case scenarios like Lockdowns where we saw many businesses going to Zero revenue overnight.

Suppose you have a Home Loan of 25 Lakhs for 25 years at 8% Interest rate and you have availed Home Loan Overdraft Facility. Your monthly EMI would be Rs. 19,295. Here is how an Overdraft facility looks like:

Above from helping during tough times, the Overdraft Balance also offsets your principal by the same amount. So essentially, you are paying lesser interest or replaying your loan faster

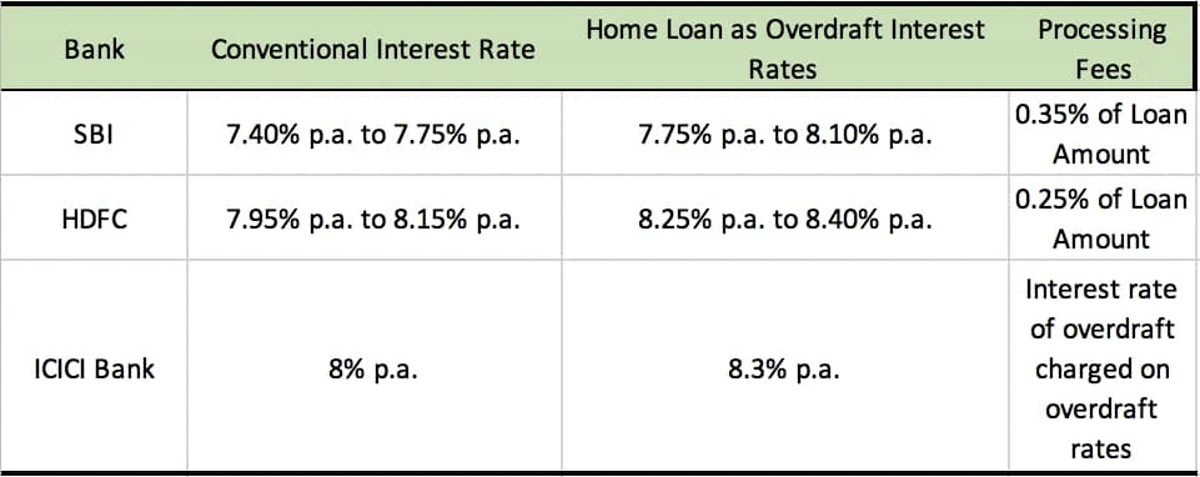

While it sounds all exciting, Do not jump for Overdraft Balance facility unless you have a very varying income stream. The interest rate of Home Loan with Overdraft Balance facility is +slightly higher+ than a conventional Home Loan. So one needs to do some calculations on an excel to figure out the true benefits of such a Facility. Also all banks have different variations in Interest rates.

Source: BankBazaar, May 2020

This is one of the most powerful weapons in your arsenal to reduce or eliminate your Future EMIs. The biggest hack is to prepay as much as possible in your earlier years of Home loan. If you are able to knock down your principal component in the first 5 years of your home loan, you can save upto 50% on your total interest payable.

Obviously one should only prepay aggressively after the individual has enough savings or emergency funds available. Every opportunity to prepay must be looked at. Are you creating a Fixed deposit as you don’t have ideas to invest? Consider prepaying the amount as your FD interest rate will always be lower than your Home Loan interest rate.

Got an unexpected annual bonus from the company for all your hard work apart from your regular Salary? A very good business month? Avoid discretionary spending and consider the Home loan pre-payment. Salary hike of 20%? Why not pay 5% extra EMI every month from the additional salary.

Be very aggressive with pre-payments in first 5 years of Loan Tenure.

Let me explain how this can be done with an example. Say you availed a home loan of Rs 25 lakh at 8% p.a. for a tenure of 25 years. Every year you managed to pay Rs. 40,000 as pre-payment for the first 5 years. This would lead to overall interest saving of Rs 6,03,264 and a reduction of loan tenure from 270 months (25 years) to 241 months, i.e., a reduction of 29 months.

We hope that the above suggestions help you to better manage your Home Loan and save on your Future EMIs. Spend a good 2-3 hours every 6 months to research and evaluate your options and don’t forget to call your banker. You would be very surprised to learn that you save a couple of Lakhs by just giving a phone call.

Do share with us your experiences in the comments below.

someone pls tell me how to save/bookmark a good topic like this

thankyou so much @nhavale . Can you please elaborate " you can buy spread to reduce interest rates whenever is applicable." as this is something that i am not aware of.

Also i understand that kotak bank will provide interest rate on repo rate where as HDFC is on RPLR (prime lending rate), will that make any difference?

thankyou so much @admin for creating this post. It was really helpful to understand how a home loan works.

I have applied for a home loan and below are the 2 options available with me and need your guidance to choose one.

Loan amount – 65lacs

Tenure – 20yrs

Offers:

HDFC – 6.7%

Kotak Bank – 6.65%

There will be no processing fee from both the institutions.

Can you please help me with one best option that i can go with? and also share some pros and cons if possible

I have Home loan with Repco Home Finance now at 10% ROI. Is there any bank accepting BT from Repco Home Finance for Patta Land(Chennai, Tamilnadu) ?

Does anyone know some info like this about credit cards due, how to reduce interest

Good n useful information

I managed to avoid taking whatever insurance they were trying to push. Now if I switch to a different bank, will they try to push the insurance thing?

Very happy to hear that it helped someone

My Uncle is going to take home loan in month of Feb 2021 & currently inquiring from different banks.

Amount of loan Required – Rs. 30 lakh; Proposal received by him are as follows:-

1) HDFC – Interest rate – 7.10%, Tenure – Min 20 years

2) PNB – Interest rate – 7.15%, Tenure – Min 15 years

3) Union bank of India – Interest rate – 7.05%, Tenure – not available

My Query is regarding 3 things, If anyone can advice it will be of great help

a) What is the minimum TENURE [loan period] offered by banks for home loan.

b) If we pay more than calculated EMI than the amount will be first adjusted with Interest component or Principal amount.

c) Are proposals received by him are in line with current market rates.

Thanks

P.S. – He has no idea/ experience whatsoever regarding any loan from any banks. Neither Do I.

Check with BOB or SBI you may get better interest rates.

A. Not sure of the min Tenure, but most people take 15 or 20-year term: HDFC has both 15 and 20 years term..

But I know a few friends who took loans for a tenure of 10 years also..

My suggestion is to take a longer period, as you can always close the loan earlier if you have money, but if you take a shorter tenure EMI will be high in case unfortunate conditions it will be difficult to pay. so Choose a longer period and do prepayment every now and then if you want.

B. Atleast for HDFC you can not pay random amounts, for prepayment you need to pay min of 3 EMIS and yes prepayment goes directly towards the Principal part only.

C, yes they are pretty much inline.

Sometimes repaying faster is not advisable….as you won’t get cash in such low rates for other purposes…so either invest or purchase the priority items (car etc., as interest is high for car loans) with the excess cash. Repay excess when your investment is not giving returns more than home loan interest…

Exactly. I have sbi max gain account. So even if I make outstanding amount to 0 by parking extra saving to maxgain, still I will not close loan account until its tenure, as in emergency situation we might not able to get immediate money at this low interest rate. Beside, we get tax exemption too

Anything for car loan?

Hi all, too bad I found this post so late.

Please, I will be grateful if you experts can help me in some way.

I got loan with HDFC of 45 lacs for a very very small property as costly as it gets in Mumbai. Last 2.5 years I am paying emi at 8.90 floating which has been set to 8. 25 now by HDFC. Property is still under construction and due in next 7-8 months. I am trying to apply for PMAY but I don’t know the actual property photos required. I went TO HDFC office last week asking for both, but they didn’t clear what kind of photos of property are required. There is no construction board at the site.

Secondly I got message from other banks like Kotak and citi asking for loan transfer at a better rate like 6.9 and 7.1 which is lot better than my current 8.25. But HDFC executive that they can give me 7.35 under interest conversion at the most that too at a cost. Then again i learnt I will lose pmay eligibility if I change. Please help some one and guide me what to do.

Its correct that if you are getting PMAY subsidy and if you transfer loan to another bank, you will lose the eligibility. Transfer of loan is considered as pre-payment by other bank on behalf of you and any pre-payment voids the subsidy, as far as i understand.

But yes, congrats that you atleast got it changed from 8.9 to 8.25. It’s a significant savings.

I have had home loans from hdfc, axis, kotak bank but none comes close to the interest rates and services offered by citi bank. Would strongly recommend to try and get your home loan or mortgage loans from citi bank. They are very selective in doing business but there’s no harm in trying. Another benifit is that they will never charge you for anything except your emi amount. No hidden charges or costs like annual maintenance charges.

Great to see that other Citibank customer also has Interest rate near 5.5%

I totally agree that Citibank has been a very good bank to deal with.

Any idea if someone has a Property insurance and also a Term insurance of loan payer attached with Home Loan (which these days are pushed compulsorily to loan seekers) and if we opt for switching Home Loan to some other Bank then will these insurances get lapsed or remain valid?

They remain valid

Go with SBI..even though I have aversion to public sector companies..wen it comes to reduction of interest rates SBI is the first one most of the times to reduce the rates.i transferred from ICICI to SBI and last tym I checked interest rate was 6.95 repo rate.Though initially you will have to visit the branch multiple times and also go to their center couple of times I think quite worth it.Also now a days they are quite active in helping you out for loan.In my case I mostly got all the forms filled through home visit.

I have a SBI home loan..is there any bank providing lesser interest charge on home loans?

Good article!

Vu

PNB is looting me on 9.55% despite being salaried and it’s my pre EMIS.

Have been paying since 3 years. Possession is due now.

And loan amount is INR 35,00,000

Need help. Can anyone suggest?

Already in process of BT with HDFCHFL for 7.20%

Any better offer?

How to complain about PNB bank? The bank had confirmed the waiver of 0.30% in June and till date they haven’t revised my interest rate despite they mailing me about the confirmation. The customer care always goes unanswered, emails go answered and resolution is 0. Tickets created on app gets automatically closed. What to do? Please suggest! Need help!

h2. Its 10.2 Lacs compare to 3.9 Lacs

In My example I reduce the tenure from 300 months to 273 months (-27 Months) and see the magic. My EMI amount it same as its is.

Think wise !!!

h2. Its 10.2 Lacs compare to 3.9 Lacs

In My example I reduce the tenure from 300 months to 273 months (-27 Months) and see the magic. My EMI amount it same as its is.

Think wise !!!

yes, Very good point and thanks for your contribution. It always helps when Dimers share their experiences… It helps all of us to save.

The only thing i would like to add, is first one must pay Higher interest loans so increasing EMI amount/lowering tenure must only be done if you have paid off higher interest loans first. So if you can pay 20k worth of loans in a month, first preference should always be as much EMI as possible on higher interest loans. But yes, if someone is keeping money in FD then lowering tenure is a magic pill

PS: Hope you wont mind if i add your screenshot to my original post. Will give you credits obviously.

I have couple of doubts, please clarify

1.Is it applicable for education loans? Bz i have a education loan and its interest rate is 10.5% in canara bank taken in 2015

For home loan…

2. Should we call bank customer care or the branch?

3. We have a home loan in canara bank was taken in 2009 and its present interest rate is 8.25%…can it be reduced still?

4. Is overdraft and OD account both are same?

1. Not sure about educational loans but no harm asking. It’s same like Mobile Data plans. If you ask/negotiate than better plans are always available to retain customers. They would not want to loose a customer for 0.2% to 0.5% but for us, it will add up to significant savings.

2. Customer care. Branch would always generally care only to get new customers.

3. Yes, for sure. Even my loan was taken in 2009 only and I use to call them often till last year.

4. yes mostly same (unless u are asking about some specific product – like savings account OD is different than Home Loan OD obviously.)

Very informative. Thanks

are you Citi Gold / private client ?

It is very helpful

I have a home loan with axis bank and received this sms in April. After that no revision done.

“Dear customer, MCLR reset effect has been passed on to your loan a/c no. XXX. Your revised ROI is 8.00 % wef 18-04-2020. Thank you.”

Please suggest if anything better can be done.

As suggested in article, Check other Loan options. Call the bank and negotiate… Tell them that you will switch, if you are not offered better interest rates… Convince them that you pay on time, you are good customer and you dont want to switch for few basis points but bank has to make it little better. Repeat every quarter.

Even if you get 0.1% to 0.2% down, You can be rest assured that you have got the sweetest deal (maybe 10-15 loots of Desidime  )

)

Great and excellent post

Thanks for sharing.

My interest rate is 7.2% in icici

Mine is at 7.4% with ICICI

what about consumer durable emi? Any news on moratorium?

{kind=link}

I have a home loan with axis bank and received this sms in April. After that no revision done.

“Dear customer, MCLR reset effect has been passed on to your loan a/c no. XXX. Your revised ROI is 8.00 % wef 18-04-2020. Thank you.”

Please suggest if anything better can be done.

As suggested in article, Check other Loan options. Call the bank and negotiate… Tell them that you will switch, if you are not offered better interest rates… Convince them that you pay on time, you are good customer and you dont want to switch for few basis points but bank has to make it little better. Repeat every quarter.

Even if you get 0.1% to 0.2% down, You can be rest assured that you have got the sweetest deal (maybe 10-15 loots of Desidime )

)